Merchant services

Payment toolkit built for your digital business. From checkout to fraud protection, all in one platform.

CHECKOUT

PAYMENT PLATFORM

PAYOUTS

FRAUD PROTECTION

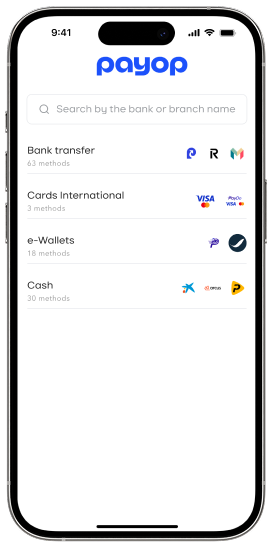

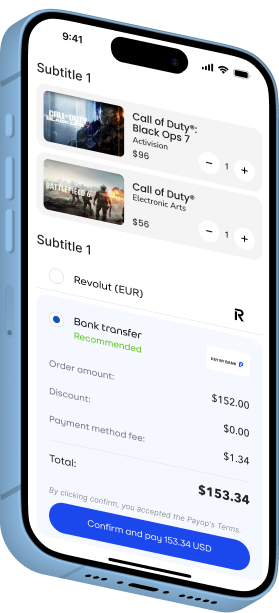

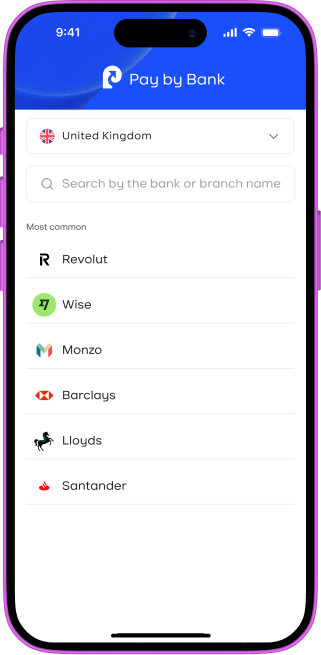

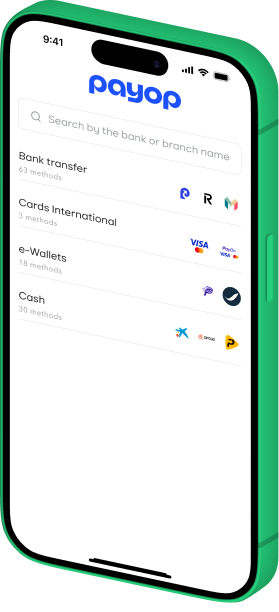

Pay by bank

Payop custom payment solution – built for speed and high conversion

-

Instant Bank Transfers

Customers pay directly from their bank accounts with real-time confirmation — no cards, no waiting.

-

Lower Processing Fees

By bypassing traditional card networks, you reduce transaction costs and improve your margins.

-

Chargeback-Resistant

With open banking, payments are reliable — meaning less fraud, fewer disputes, and lower risk for your business.

-

Secure & PSD2-Compliant

Built on open banking APIs across Europe and the UK, with strong customer authentication (SCA) by default.

Get started in just 4 steps

Fill out a short pre-check form

Get your custom offer

Pass verification

Integrate and go live

Who we serve

Payment cheat-code for digital-first businesses

Gaming

Let players worldwide pay seamlessly — without chargebacks, blocked accounts, or payout delays.

Discover Payop for Gaming →

Digital goods

Sell gaming items, software, gift cards, and other digital goods globally with secure, instant payments.

Discover Payop for Digital Goods →

E-commerce

Boost conversion in your online store

with direct-to-bank payments

and lower fees.

iGaming

Enable fast deposits and instant payouts for betting and online casinos — fully compliant and secure.

Discover Payop for iGaming →

Testimonials

Trusted by 10,000+ digital businesses

"Everything, starting from the integration process, was very clear and direct. Secure payments, fewer failed transactions, effective support, assistance with chargeback handling – all processes are running smoothly."

"Onboarding went extra quick, with no unnecessary paperwork or repetitive requests. It genuinely feels like the team knows what they are doing and understands the specifics of our business are. That’s not something you see very often."

"We saw an immediate boost in successful transactions, especially for international customers."

"For a global business like ours, having one payment service provider that covers so many countries is a huge advantage. And Payop clearly understands the markets we operate in. The payment methods they suggested actually convert."

"Easy set-up, great coverage and payment method list, especially considering the unified integration. Interface is easy to navigate, good reporting tool, and we also love the team-member access settings. Delegating tasks without compromising control has made our workflow much smoother."

"Since switching to Payop, our payment-related support tickets have dropped by nearly 40%. It's been a huge relief for our team."