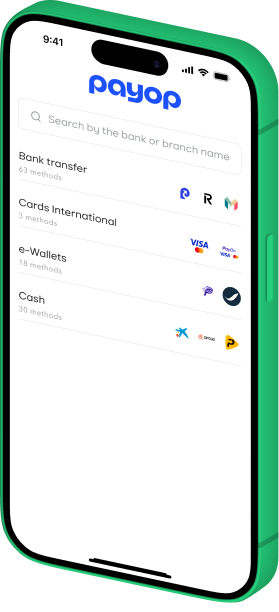

Merchant services

CHECKOUT

PAYMENT PLATFORM

PAYOUTS

FRAUD PROTECTION

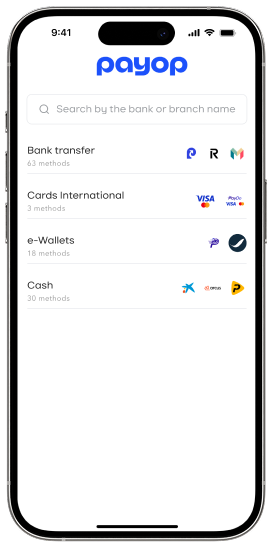

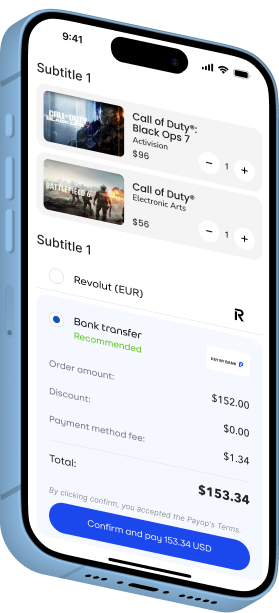

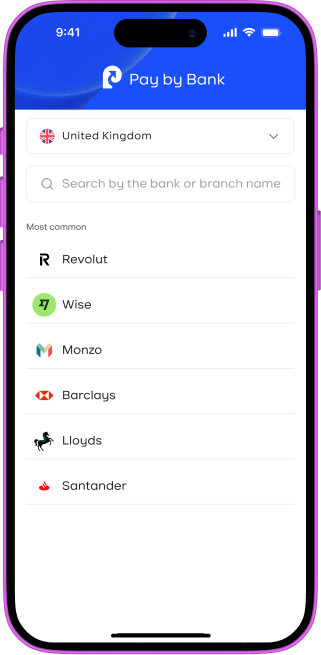

Pay by bank

-

Instant Bank Transfers

Customers pay directly from their bank accounts with real-time confirmation — no cards, no waiting.

-

Lower Processing Fees

By bypassing traditional card networks, you reduce transaction costs and improve your margins.

-

Chargeback-Resistant

With open banking, payments are reliable — meaning less fraud, fewer disputes, and lower risk for your business.

-

Secure & PSD2-Compliant

Built on open banking APIs across Europe and the UK, with strong customer authentication (SCA) by default.

Get started in just 4 steps

Fill out a short pre-check form

Get your custom offer

Pass verification

Integrate and go live

Who we serve

Gaming

Let players worldwide pay seamlessly — without chargebacks, blocked accounts, or payout delays.

Discover Payop for Gaming →

Digital goods

Sell gaming items, software, gift cards, and other digital goods globally with secure, instant payments.

Discover Payop for Digital Goods →

E-commerce

Boost conversion in your online store

with direct-to-bank payments

and lower fees.

iGaming

Enable fast deposits and instant payouts for betting and online casinos — fully compliant and secure.

Discover Payop for iGaming →