Sep 10 4 MIN READ

People are increasingly paying for their daily expenses with e-wallets on their phones rather than cards or cash. For some, it’s just safer and more convenient, while others simply don’t have access to traditional card payment methods.

But as digital wallets become more common across emerging markets, a critical question arises for online businesses: Are they enough?

Relying on a single payment method, no matter how popular, can limit reach, reduce conversions, and leave out entire customer segments. To truly succeed in these regions, businesses need to offer a payment mix that reflects local realities, not just global trends.

E-wallets are quickly becoming the go-to way to pay online, particularly in emerging markets. By 2030, they’re expected to account for 65% of all global e-commerce payments. That’s a huge leap, showing just how far mobile payments have come.

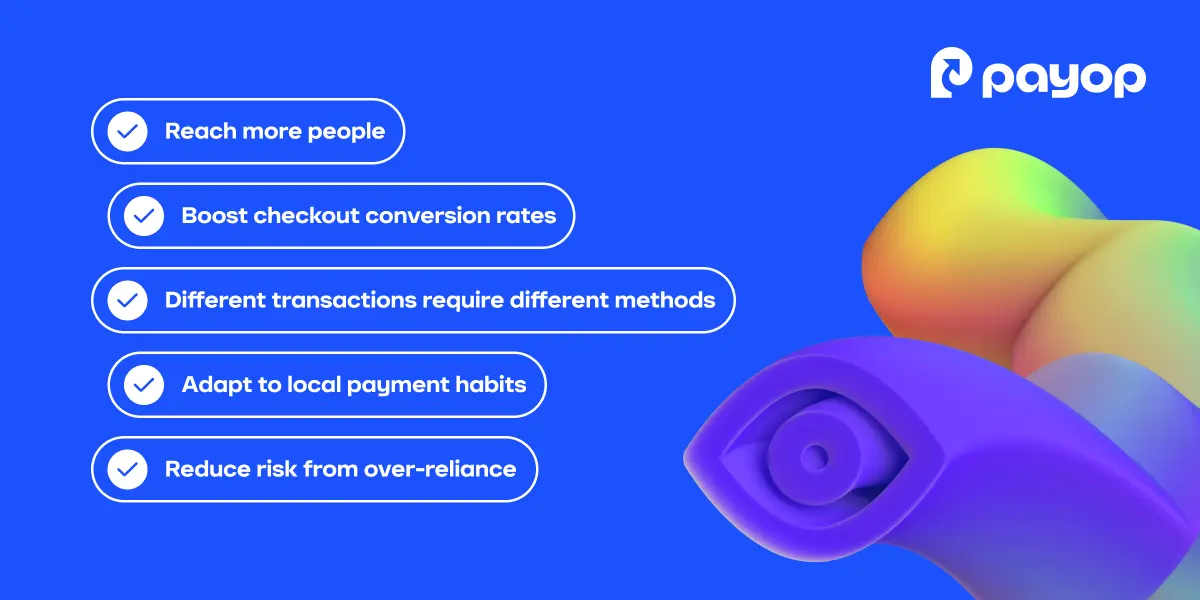

There are a few clear reasons for this growth:

For millions, mobile wallets are the easiest and safest way to pay. However, as their popularity keeps growing, relying only on e-wallets can leave gaps, especially in markets where other methods like cash or bank transfers are still widely used.

Learn about digital wallet boom in Latin America.

Even in mobile-first regions, not everyone uses e-wallets, and not every purchase is made through one. Here’s why offering just one or two payment options can be risky:

Not everyone uses an e-wallet. Some shoppers prefer to pay with cash at a local store, others trust their bank apps more, and many don’t have access to digital wallets at all. A limited payment setup means leaving those customers behind.

When customers don’t see a familiar payment option, they often don’t complete the purchase. Offering a mix of trusted local methods, like cash vouchers, bank transfers, or regional cards, can reduce drop-offs and increase completed transactions.

E-wallets may be perfect for low-cost, everyday purchases. But for larger transactions, like booking a flight or buying electronics, people often prefer options like bank transfers or instalment plans. Businesses need to support both to meet the varied needs of their customers.

Each market has its own mix of preferred methods. For example, Pix dominates in Brazil, SPEI in Mexico, and cash is still widely used in parts of Africa and Southeast Asia. Tailoring your payment mix to these habits shows your business understands the local environment and builds trust.

If your checkout depends entirely on one e-wallet provider, a single outage or policy change can disrupt your entire operation. A more diverse setup ensures your business stays stable and accessible, no matter what.

The goal isn’t to support every payment method in the world, but to offer the right mix for each market. That could include:

Offering multiple options helps remove friction at checkout and builds trust with your customers wherever they are.

Here’s how to make sure your business is offering payment options that truly work in each market:

Payop connects you to 500+ payment methods in 170+ countries, including local wallets, real-time transfers, and cash-based options. Whether you’re targeting customers in Southeast Asia, Latin America, or Africa, we help you build a payment setup that feels local.

And with real human support, we make sure your payments work just as smoothly as your business.