Apr 03 7 MIN READ

To scale in Europe, you need to understand local payment method preferences. Apart from demands for high security and user-friendly checkout, other factors are shaping European markets in 2026.

In this article, we break them down. Discover the key online payment trends across the EU’s top markets and learn how to build a checkout that truly converts.

From the Nordics to Italy, advanced banking and high smartphone use define the European payment landscape. That’s why cards, bank transfers, and digital wallets drive e-commerce here. Another important factor – financial regulations. The Instant Payments Regulation, for example, sets the standard for instant bank transfers at 24/7 availability and 10-second processing. As a result, Pay by Bank becomes the continent’s top trend.

The European Payments Initiative created Wero, a mobile payment system based on Pay by Bank technology. It is designed to become the standard payment method across the EU, replacing local systems such as Germany’s Giropay and France’s Paylib. As a Pay by Bank, Wero moves funds directly between accounts in real time, bypassing card networks entirely – a step towards Europe’s independence from Visa and Mastercard.

Payop has its own Pay by Bank. Driven by open banking technology, this secure solution lets customer pay directly from their banking app, lowering the risk of data breach.

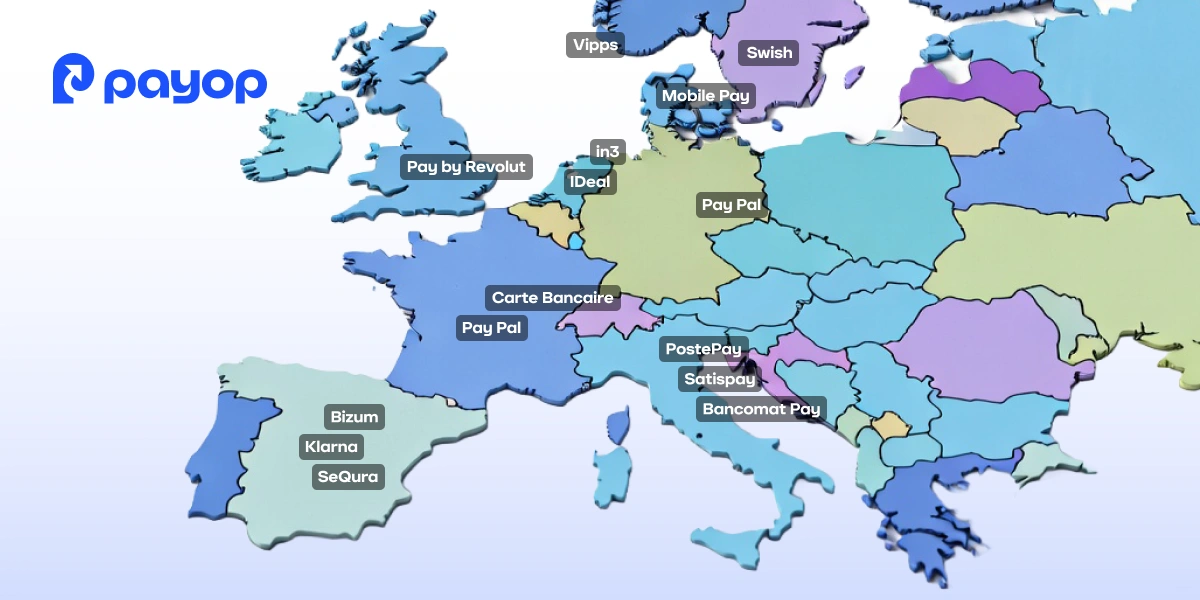

Beyond general trends, each country has its own deep-rooted cultural habits and local laws. They play a key role in shaping preferences for payment methods. For example, while some markets quickly accept innovations like Pay by Bank, others still rely on traditional cards or cash for in-person shopping. On top of that, there are popular local solutions, such as iDEAL in the Netherlands and Swish in Sweden.

To better understand this landscape, let’s have a closer look at the most popular payment options in Europe’s top markets.

According to the EHI Retail Institute, PayPal remains the German market’s leader due to its customer protection. Users feel safe knowing they can get a full refund if the order didn’t arrive or doesn’t match their expectations. Another reason why Germans trust PayPal: it keeps payers’ sensitive data off a merchant’s systems. While Apple Pay and Google Pay are booming with Gen Z, PayPal remains the top one-click payment method for the rest, thanks to its security and convenience.

The French market relies mostly on the national card scheme, Carte Bancaire (CB). With 77 million cards in use, most of which are co-branded with Visa or Mastercard, CB allows both domestic and international shopping. According to the FEVAD 2025 report, 89% of customers prefer cards, while 46% regularly use e-wallets for online payments, including PayPal.

France is also no stranger to Pay by Bank. For years, they used a national solution called Paylib, which Wero officially replaced in 2026. But for e-commerce, Payop’s Pay by Bank is a go-to alternative. No manual data entry makes checkout frictionless – French customers simply choose the familiar bank and pay in seconds.

Unlike their neighbours, the British rely almost exclusively on Mastercard and Visa. Card payments dominated 64% of the UK market in 2024, with forecasts reaching 67% by 2034. Under Section 75 of the Consumer Credit Act, the credit card issuer is legally responsible if a merchant fails to fulfil the order between £100 and £30,000. Thanks to this, credit card usage is very popular in this region.

At the same time, the UK remains a global leader in open banking adoption. Here, all banks operate under the unified API standard created by the OBIE (Open Banking Implementation Entity). This makes Pay by Bank much easier and cheaper for businesses to set up and use.

Since 2005, iDEAL has dominated the Dutch market. In 2026, this real-time bank transfer system completed its transition to Wero. This unified solution maintains the near-instant speed of transaction processing while adding Wero’s payer protection and cross-border payments.

Despite the Dutch traditionally avoiding debt, buy now, pay later (BNPL) is gaining popularity among younger generations. Local services like in3 are common because they let customers pay in three steps without extra costs – a perfect payment method for the pragmatic Dutch mindset. In this landscape, Visa and Mastercard remain a secondary option, typically reserved for international travel or high-value purchases.

The Nordic region leads the West in the adoption of alternative payment methods (APMs). In 2026, the top three systems dominate the payment landscape: Swish in Sweden, Vipps in Norway, and MobilePay in Denmark and Finland. A2A payments power these wallets, which were originally built as private bank networks. Today, they represent the most successful equivalent to open banking worldwide.

The Nordics are building their own Pay by Bank ecosystem. As Vipps and MobilePay merged into a single company, a resident of Helsinki can now send money to a friend in Oslo or Copenhagen via phone number as easily as they would domestically. Swish currently remains independent, but actively collaborates with this unit through EMPSA (the European Mobile Payment Systems Association).

Local card schemes such as Denmark’s Dankort and Norway’s BankAxept play a major role in their domestic markets. As for international payments, locals still rely on Visa and Mastercard.

In 2026, Bizum is the most preferred online payment method in Spain. This is a national Pay by Bank solution that Spaniards completely trust for everything from local shops to major e-commerce sites. For most businesses, Bizum offers lower fees than traditional card payments, especially for small- to medium-sized transactions.

Spanish customers are used to the speed and convenience of Bizum. In addition to this payment method, they also use digital wallets. Apple Pay and Google Pay are now the go-to choices for mobile users, while PayPal remains popular for its extra customer protection. For larger purchases, many locals prefer BNPL services like Klarna or the homegrown favourite, SeQura.

In 2026, cards remain the primary choice for most Italians, with PostePay leading the charge. Issued by the national postal service, PostePay prepaid cards are co-branded with Visa and Mastercard. Users can top up specific amounts and shop online, keeping their primary bank accounts isolated from the internet for added security. Now, PostePay handles nearly 25% of all digital transactions in Italy – a larger share than any single traditional bank.

Another trend is the growing popularity of APMs. Satispay, in particular, stands out as an independent digital wallet that enables direct account-to-account transfers. Its competitor is Bancomat Pay, the digital evolution of Italy’s traditional PagoBancomat network. This solution is built directly into banking apps, allowing users to pay or send money with just their phone number. Bancomat Pay’s partnership with Visa now allows Italians to use contactless payments abroad.

The key takeaway is clear: Visa and Mastercard are still popular, but Europe is moving toward alternative solutions. Through their local national schemes, European customers are used to high security and speed of real-time online transactions. And they now expect the same seamless experience from your checkout.

Payop helps you meet these expectations. We support payment methods Europeans already know and trust, including the Dutch iDEAL and Pay by Revolut, which is a favourite in the UK. And with our Pay by Bank solution, you can offer European customers the speed, top-tier security, and frictionless checkout they appreciate.

What are the benefits of this payment method for your business?

Contact our team at sales@payop.com to learn more.