Mar 20 6 MIN READ

When expanding into new countries, there are many factors to consider. One of the most important is choosing the right set of payment methods for each market.

There’s no room for guesswork, as a wrong choice can hurt your revenue. But how do you know which online payment options to offer in each region, and what determines whether it’s suitable or not?

In this guide, you’ll discover the main factors that help you choose the best options for your payment strategy.

Let’s face it: if you want to expand internationally, a one-size-fits-all approach to online payments isn’t the most successful path. Just adding the most popular options to the checkout page might seem like a safe bet. But in reality, it’s not that simple.

Imagine that you’re going to see a highly anticipated movie. You arrive at the cinema in France, ready to buy a ticket, only to learn the screening is in Mandarin Chinese with Spanish subtitles. You’re told that those languages are the most widely spoken in the world, so the cinema expects to reach the broadest possible audience. But you’re in France, where people speak French. You don’t understand a word of Chinese or Spanish. Most likely, you wouldn’t buy the ticket; you’d walk away, frustrated that you couldn’t watch the movie.

The same principle applies to digital payments. While credit and debit cards are popular in many countries, in some regions, traditional banking is limited, expensive, or hard to access. Just like in the cinema example, if you rely on card payments in underbanked markets, many local customers simply won’t be able to pay.

On top of that, payment preferences vary by region. Shoppers follow established habits and stick to methods they know and trust. If you ignore this, we have bad news: succeeding in new regions won’t be easy.

When you enter new regions, you shouldn’t count on the same set of payment methods everywhere. But adding every possible option isn’t a good strategy either. Work smarter, not harder, and choose the payments that best fit your customers.

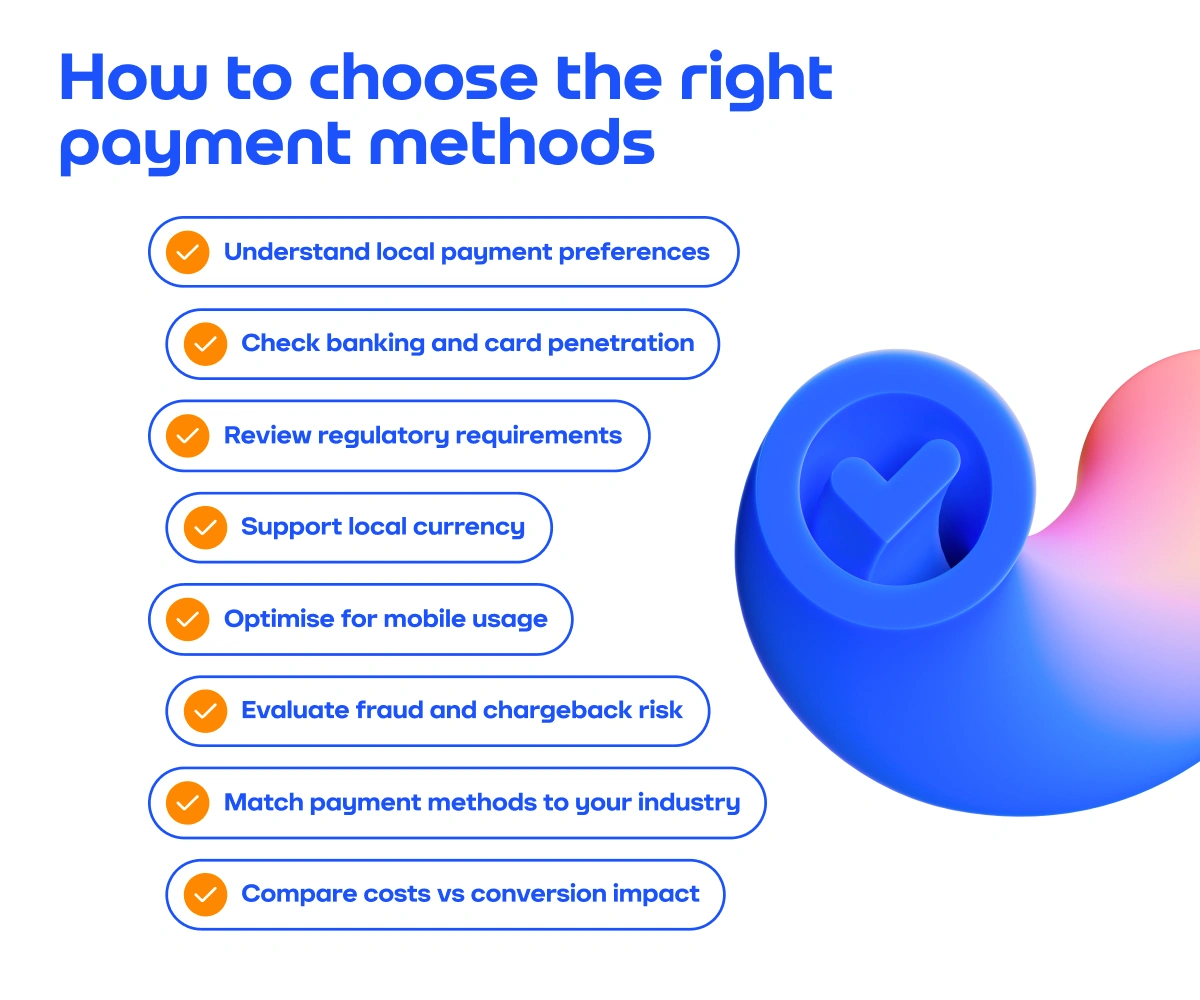

To understand if a payment method works well for a certain country, consider:

The first question to ask: Can local customers actually use this method in their country? Take Latin America: it’s a fast-growing, highly promising market with strong revenue potential for online businesses. At the same time, LATAM remains widely underbanked. Adding only card payments at checkout for a market like this won’t pay off. In contrast, digital wallets and cash-based vouchers are very common across this region.

Smartphone penetration and the stability of the internet connection also play a role. You clearly can’t rely on smartphone-based wallets in regions where most people don’t have a smartphone. For countries with slow internet, it’s better to offer payment options that work even with poor connectivity. Examples include prepaid vouchers and USSD-based mobile money.

Just because a payment method is available in the country doesn’t guarantee it’s the right fit. Why? It all comes down to trust.

Some shoppers feel confident paying directly from their banking app, while others prefer well-known wallets like PayPal. And in certain countries, users trust only local solutions.

How can you tell if customers trust a payment method? The answer is very simple: if people use it often, that’s a strong sign of trust. To gain clear insights into usage statistics, refer to local e‑commerce research, surveys, and fintech reports. And to make things easier, partner with an experienced payment service provider that understands the ins and outs of different markets.

Take a close look at how your customers actually shop. Do they mostly browse on mobile or stick to desktops? Are their purchases quick impulse buys or planned big orders? Keep their habits in mind when designing your payment setup, or you risk losing conversions.

For mobile-first regions, add digital wallets with biometric authentication, and avoid long card forms that slow users down. If repeat purchases are common, one-click payments will make the process much easier for customers. And for markets with high average order value (AOV), solutions such as buy now, pay later (BNPL) usually work well. They allow splitting large transactions into smaller ones, making bigger purchases more manageable for customers.

Regulations play a big role in determining which online payments you can offer and how they work. Some countries require extra authentication for digital payments, while others expect providers to hold a local license. On top of that, rules on currency conversion, cross-border transfers, and data storage can change how a payment method functions in a market.

Then there are rules tied to specific methods. For example, BNPL services are treated as consumer credit and must follow local lending laws. Real-time bank transfers often need a direct connection to the local banking system. And in certain regions, anti-money laundering (AML) rules can limit voucher-based payments.

Alternative payment methods (APMs) are no longer optional – they are key to international expansion. Today, customers expect speed, safety and convenience from online payments. And in many regions, APMs meet those expectations, winning over traditional systems.

Alternative payment methods are digital solutions that let users send, receive, and spend money without relying only on cash and cards.

They include:

Adding these alternative solutions will help you adapt to local payment preferences and maximise conversions in different regions.

And here’s how:

Selecting the right digital payment solutions isn’t easy – there are lots of options, local habits, and regulations to navigate. Researching all this for each new market takes time, and every mistake can cost you revenue. That’s where a payment service provider (PSP) becomes your irreplaceable strategic partner.

At Payop, we know which payment methods are trusted in each region and can help you maximise your checkout conversion. We offer 500+ payment methods, including local options, and 100+ currencies across 170 countries.

On top of that, you’ll get:

Ready to scale into new markets? Contact our team at sales@payop.com to learn more.