Africa’s digital payments landscape is growing at full speed. From mobile money to fintech innovations, the continent is embracing digital finance like never before. But with that growth comes complexity. Every country has its own set of rules, making Africa one of the most diverse regions in the world in terms of payment regulations.

If you’re a business expanding into Africa – or already operating across multiple countries – you’ll need a clear understanding of how these regulations work. Let’s break it down.

Diverse African regulatory environment

Unlike the EU’s unified PSD2 or some regional frameworks in Latin America, Africa is made up of dozens of separate regulatory environments. Each country’s central bank or financial authority sets its own rules on payments, e-money, and fintech.

Here are some of the main regulators:

Nigeria – Central Bank of Nigeria (CBN)

South Africa – South African Reserve Bank (SARB) and Financial Sector Conduct Authority (FSCA)

Kenya – Central Bank of Kenya (CBK)

Ghana – Bank of Ghana (BoG)

Francophone West Africa – BCEAO (Central Bank of West African States)

Egypt – Central Bank of Egypt (CBE)

These institutions control who can offer financial services, what licenses are needed, how customer data is handled, and how anti-money laundering rules are enforced.

Mobile money and e-money regulations

Mobile money is a massive part of Africa’s financial story. It’s what brought financial access to millions, and regulators have built specific frameworks around it, usually classifying it under Electronic Money Issuers (EMIs).

Kenya – Central Bank of Kenya (CBK)

Regulated under the E-Money Guidelines (2013)

Mobile money providers must be licensed as Electronic Money Issuers (EMIs)

Customer funds must be safeguarded in segregated trust accounts

Monthly reporting and real-time transaction monitoring are mandatory

CBK has made interoperability between providers a legal requirement

Nigeria – Central Bank of Nigeria (CBN)

Introduced a Payment Service Bank (PSB) framework to expand access in rural areas

PSBs can provide wallets, transfers, and savings accounts, but cannot offer credit or forex

Must keep 75% of customer funds in treasury instruments

Minimum capital requirement: ₦5 billion (approx. $10 million)

Nigeria also uses a tiered KYC system:

Tier 1: name and phone number (low limits)

Tier 2 & 3: government ID and address verification (higher limits)

As the fintech sector grows, African regulators are adapting with new licensing regimes to cover digital services like wallets, gateways, and processors. Open banking is also starting to appear on the radar.

Transfers between African countries are often slow and expensive, particularly when using different currencies. In response to this problem, regional initiatives are emerging to simplify and localise cross-border payments.

PAPSS – Pan-African Payment and Settlement System

Backed by the African Export–Import Bank (Afreximbank) and the African Union

Enables real-time cross-border payments in local currencies

Connects African central and commercial banks to eliminate reliance on foreign clearing systems

Already operational in the West African Monetary Zone (WAMZ)

AfCFTA – African Continental Free Trade Area

The largest free trade area in the world by number of countries

Aims to standardiыe financial rules and mutually recognise licenses

Encourages collaboration on KYC norms, data protection, and fintech regulation

Still in early implementation, but presents long-term harmonisation potential

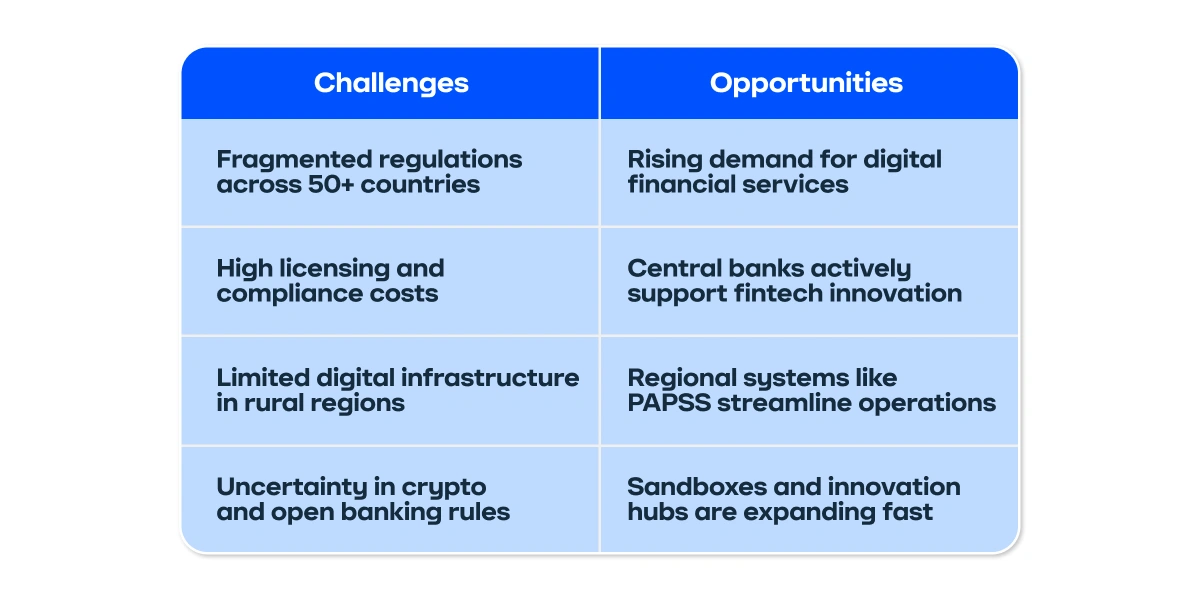

Challenges and opportunities in Africa

While Africa’s payment ecosystem holds immense potential, navigating it isn’t without its difficulties. Regulatory fragmentation, infrastructure gaps, and compliance costs pose real challenges for businesses. At the same time, the continent offers unmatched opportunities for innovation, financial inclusion, and cross-border growth. Here’s a look at what companies need to consider:

Final thoughts

Africa’s regulatory landscape may be fragmented, but it’s also full of promise. As fintechs and mobile payment services continue to shape the future of finance, regulators are catching up with clearer, more supportive frameworks.

For businesses to succeed in the region, they need to:

Understand each country’s requirements

Build strong compliance systems

Partner with local experts or providers that can ensure regulatory alignment

By doing so, companies can tap into one of the world’s most dynamic and fast-growing digital economies responsibly and sustainably.