Jul 17

5 MIN READ

In Brazil, more people now use Pix than credit cards. In India, UPI processes over 10 billion transactions each month more than Visa and Mastercard combined. Around the world, real-time payments are not just gaining ground. They're becoming the default way to pay.

Real-time payment (RTP) systems are reshaping financial ecosystems and raising the bar for speed, transparency, and efficiency. In this article, we explore how they work, where they thrive, and how they can benefit your business.

Real-time payments are digital transactions that are completed initiated, cleared, and settled in seconds. They`re available 24/7, including weekends and holidays, offering instant confirmation to both the sender and the receiver.

Key advantages include:

Instant settlement and access to funds

Improved user experience and trust

Reduced reliance on cash and traditional cards

Lower fees and operational costs for businesses

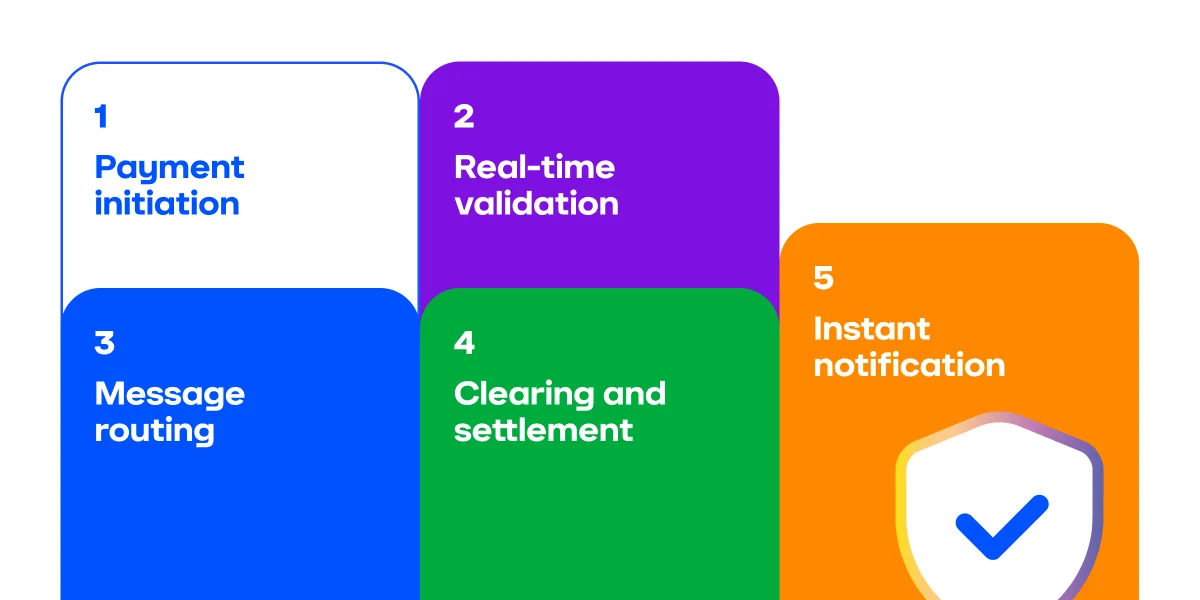

Real-time payments may seem simple: you send money, and it arrives instantly. But behind the scenes, a lot happens in just a few seconds. Here's how the process typically works:

1. Payment initiation

The user starts the transaction through a bank app, payment service, or digital wallet by entering a phone number, scanning a QR code, or selecting a merchant.

2. Real-time validation

The system checks if:

The sender has sufficient funds

The receiver`s account is active

The request is legitimate (using fraud filters, biometrics, or two-factor authentication)

This happens almost instantly, thanks to fast and secure APIs.

3. Message routing

The payment request is routed through a central infrastructure, usually run by a central bank, clearing house, or a regulated third party (e.g., NPCI in India and Banco Central do Brasil for Pix).

4. Clearing and settlement

Unlike traditional batch payments, RTP systems:

Clear the payment by verifying both sides and updating balances

Settle it in real time by moving funds between bank accounts

In many systems, settlement happens through a central account ledger, often backed by the central bank.

5. Instant notification

Both parties are notified immediately, confirming that the money has been transferred and received successfully.

In their work, RTP systems rely on the following technologies:

Open APIs, which enable fast communication between banks and apps

ISO 20022 a global standard for data-rich transactions

Alias mapping services, which allow payments by phone or ID instead of bank account numbers

Real-time fraud detection that uses machine learning or rule-based systems to block suspicious activity instantly

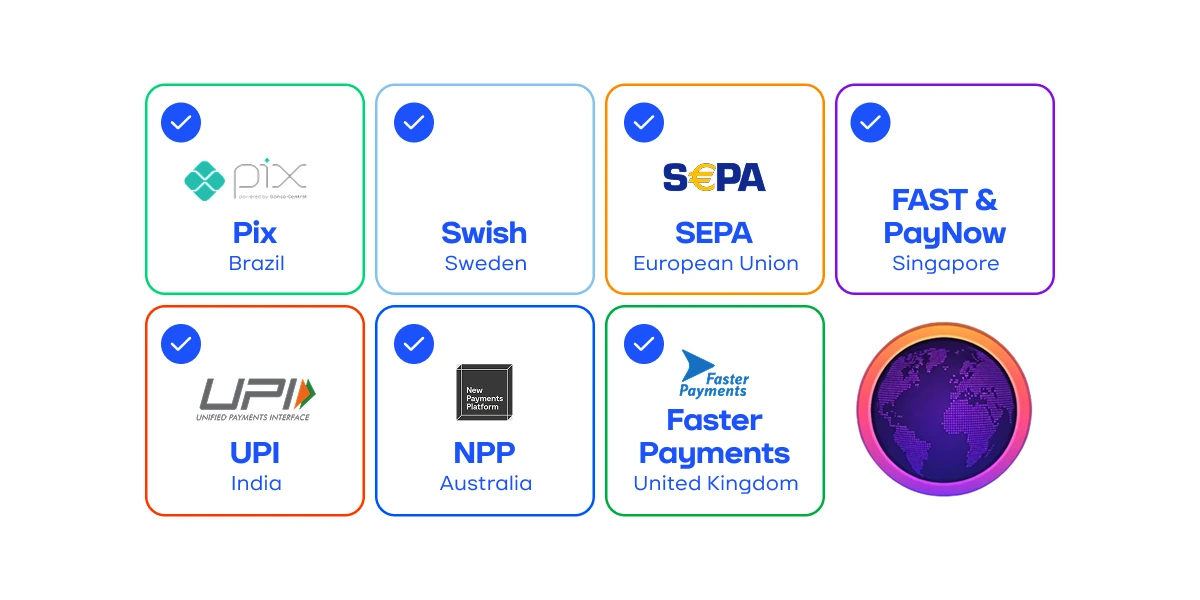

Launched in 2020 by the Central Bank of Brazil, Pix quickly became the dominant payment method in the country. As of 2025, over 150 million users make billions of Pix transactions monthly, covering everything from P2P transfers to utility payments and business transactions. It supports payments via QR codes, phone numbers, and national IDs, and is free for individuals.

SEPA Instant allows to make euro-denominated payments within 10 seconds across participating European countries. Over 29 countries are part of this scheme, with increasing merchant and fintech adoption, especially as the EU mandates wider use of instant payments by 2025.

The UK`s Faster Payments Service (FPS), launched in 2008, was one of the earliest RTP systems. It enables near-instant domestic transfers between banks and has been widely adopted for personal and business use, with support from banks, fintechs, and payment service providers.

Find out about payment regulations, trends and popular methods in the UK.

Launched in 2012 by Swedish banks and the central bank, Swish allows instant transfers between users and businesses using just a phone number. It's widely adopted in Sweden for peer-to-peer transfers, retail payments, donations, and even invoices. Around 80% of Swedes use Swish, making it a national standard for real-time mobile payments.

UPI, launched in 2016 by the National Payments Corporation of India (NPCI), allows users to link multiple bank accounts and make real-time payments through a single mobile app. UPI supports both small-value and high-value payments, with over 10 billion monthly transactions recorded in 2024. It`s also being adopted for cross-border use in countries like Singapore and the UAE.

Australia`s NPP supports instant transfers and data-rich transactions. Services like Osko leverage NPP to facilitate consumer and business payments, and real-time payroll, invoicing, and e-commerce integrations are growing rapidly.

Singapore`s FAST (Fast and Secure Transfers) supports real-time bank transfers, while PayNow allows users to send funds using just a phone number or national ID. Singapore has also pioneered international RTP interoperability with India and Malaysia.

For businesses, real-time payments offer more than speed. They bring efficiency, cost savings, and a better customer experience.

Here`s what merchants gain:

Immediate access to funds no more waiting days for settlement

Faster order processing thanks to instant confirmation

Lower payment costs by avoiding card networks and their fees

Fewer chargebacks and reduced fraud risk

Happier customers who can pay the way they prefer

In markets like Brazil and India, offering RTP methods like Pix or UPI is no longer optional it`s expected.

Getting started with real-time payments doesn`t have to be complicated. With Payop, merchants can tap into local RTP systems across multiple countries through a single integration.

Here`s what Payop offers:

Access to Pix, SEPA Instant, and other regional methods

Faster processing, improving your cash flow

Lower fees compared to cards and wire transfers

An all-in-one dashboard to track payments, payouts, and customer activity

Dedicated support manager who actually helps rather than hides behind standard guidelines

Whether you sell digital goods, run a gaming platform, or operate an online marketplace, Payop helps you accept the payment methods your customers already trust, wherever they are.