Feb 20 6 MIN READ

Each year, the e-commerce industry loses billions of dollars to chargebacks. However, their impact goes way beyond lost revenue. The true danger is high chargeback rates. They can cause card network penalties, harm your reputation, and even affect your ability to accept online payments.

In this article, we explain what chargebacks are, what triggers them, and how to protect your business.

Chargebacks happen when a customer contacts their bank rather than the merchant to reverse a payment. In this case, the bank withdraws the disputed amount from the merchant’s account, temporarily refunds it to the customer and investigates the matter.

There are two possible outcomes. In the first case, the merchant wins the dispute, and the funds are returned to his account. In the second case, the customer’s claim is proven legitimate, and the refund becomes permanent. The merchant loses the funds, pays the chargeback fee, and the dispute is counted toward their chargeback ratio.

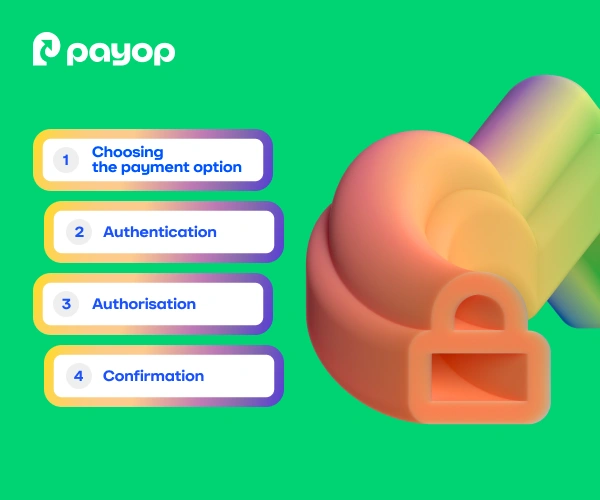

From the customer’s perspective, a chargeback may look simple. In reality, it consists of many steps, involves several parties, and can take weeks.

Let’s break down this process:

A chargeback begins when a customer contacts their bank to dispute a transaction and formally request their money back.

The payer’s bank reviews the claim and sends the chargeback request to the merchant’s bank via the card network. At this stage, the customer’s bank may issue a temporary refund to the cardholder while the investigation is still ongoing. The acquiring bank then withdraws the disputed amount and chargeback fees from the merchant’s account.

The notification includes chargeback information, such as transaction details, reason code, disputed amount and fees, response deadline, and instructions for submitting evidence. After this, the merchant has two options: accept the chargeback or challenge it.

If the merchant decides to challenge the dispute, collecting as much evidence as possible is very important. It may include purchase and payment records, delivery confirmation, the customer-signed return policy, and any customer correspondence.

The issuing bank reviews the customer’s claim and the merchant’s evidence. Based on this and the card network rules, the bank makes a decision.

If the merchant wins the dispute, the funds are credited back to their account. If the bank approves the chargeback, the refund becomes permanent, and the business loses the disputed amount, along with the chargeback fee. In addition, every chargeback increases the merchant’s chargeback ratio.

When a business or customer disagrees with a decision, they may escalate the dispute. But because arbitration is costly and slow, it’s rare.

Both refunds and chargebacks mean returning money to a customer. The difference lies in two aspects:

A refund is initiated by the merchant and processed by the payment provider when a customer requests their money back directly from the website. A chargeback is initiated by the customer through their bank. It triggers a formal dispute and may result in additional fees and a negative impact on the merchant’s chargeback ratio.

Refunds usually settle within a few days.

Chargebacks can take weeks or months and require evidence, formal responses, and follow-ups. As a result, disputes lead to higher costs, more administrative work, and greater long-term risk than standard refunds.

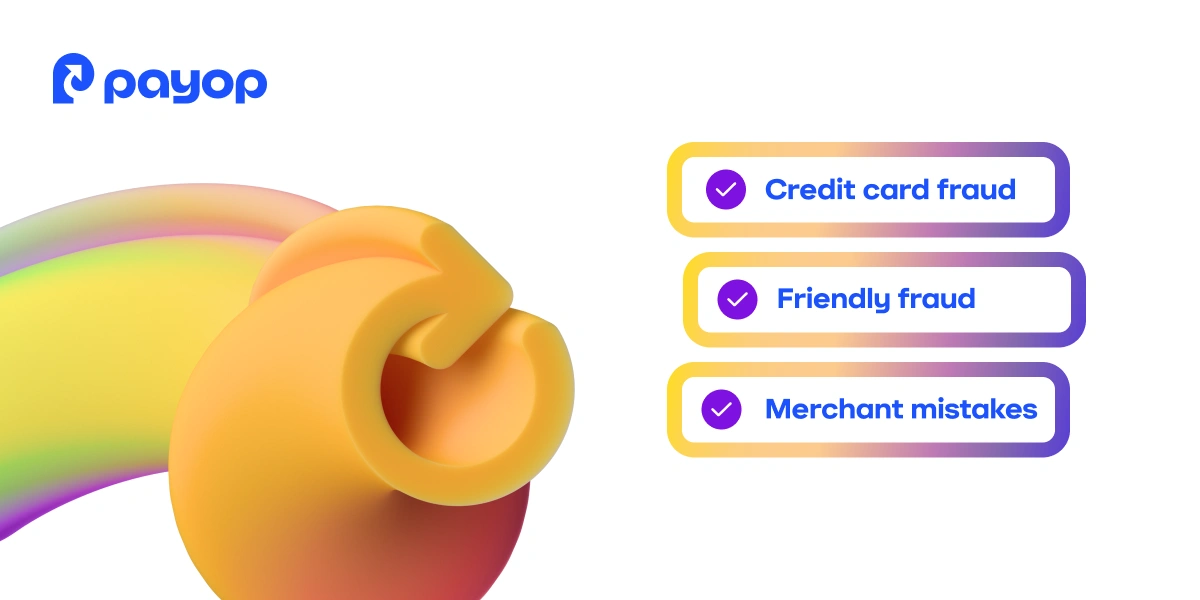

Cardholders can request a chargeback for three main reasons:

In these cases, the transaction was never authorised by the cardholder. Fraudsters may get card details through phishing, malware, data breaches, or lost physical cards. When the customer notices strange unauthorised transactions, they contact their bank. The bank then investigates the case. If the fraud is confirmed, the bank will return the money to the customer.

In so-called friendly fraud cases, the payer authorised the transaction but later disputes it.

Typical scenarios include:

Friendly fraud can also happen by accident. For example:

Sometimes, disputes happen because of transaction errors or merchant mistakes.

Examples include:

Chargebacks are costly, but their impact goes beyond lost revenue and extra fees. Repeated disputes raise your chargeback rate. If it goes over 1%, you may face penalties, higher processing costs, or mandatory monitoring. In the long run, your business can lose its merchant account and the ability to accept card payments.

You can’t avoid chargebacks entirely, but the right setup can reduce the risk. Here’s what you can do to protect your business:

To minimise the risk of unauthorised transactions:

Payment disputes are stressful, time-consuming, expensive, and harmful to your reputation. But working with a payment service provider such as Payop makes a difference.

We help merchants manage chargebacks by clarifying dispute reasons, supporting evidence preparation, and reducing avoidable losses. Even better, with our Pay by Bank solution, many disputes can be prevented altogether. It practically eliminates chargeback risk as customers approve payments directly in their banking apps. There’s just no room for unauthorised transactions and friendly fraud left.

If you want a reliable and secure payment partner, contact us at sales@payop.com to learn more.